We must appreciate the efforts of government of India for timely decision on additional capacities of urea. Around 7.62 million tons capacities will be added. Out of which 6.35 million tons (3 Urea plants of HURL, Matix & Ramagundam) will be added in 2021 -22 and Talcher Urea plant is expected within next 3-4 years.

Will this addition suffice the India demand of Urea? Or India dependency on imports will remain same. Should India plan to add more capacity and is this right time to think on this? Which zone of India will be most sufferer in next 5 years?

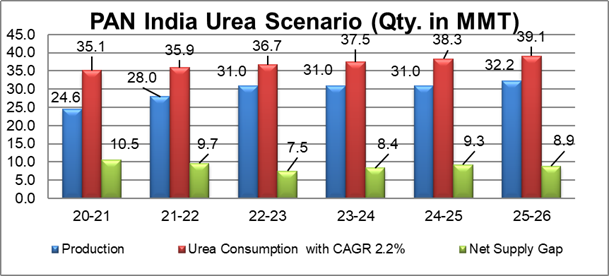

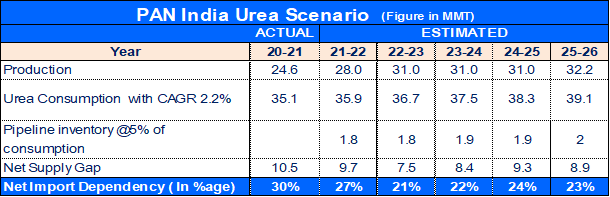

If we see PAN India scenario for next 5 years, Urea production will increase by 31% from 24.6 Mn tons to 32.2 Mn tons and demand will also increase by 11.5% i.e. 4 Mn tons by 2025-26, with a CAGR of 2.2% (from 35.1 Mn tons to 39.1 Mn tons). This indicate that India dependency will be remain same around 20 – 25%, even after adding 6 Urea plants including Talchar.

Regional / Zone Urea Balance in India

We must appreciate the efforts of government for giving green signal for revival of various old urea units and support industry for new investment. With their initiatives, India will add 7.62 million tons urea capacity which is around 22% of urea demand in 20-21. This will definitely reduce dependency on urea imports. PAN India dependency will reduce from 30% to 23% in next 5 years with consideration of increased demand with a CAGR of 2.2%.

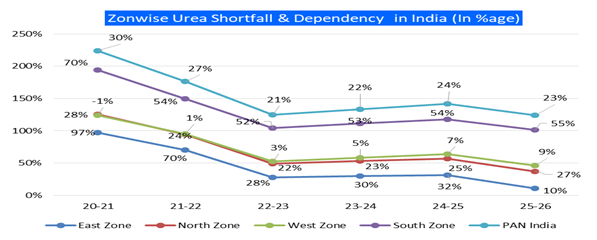

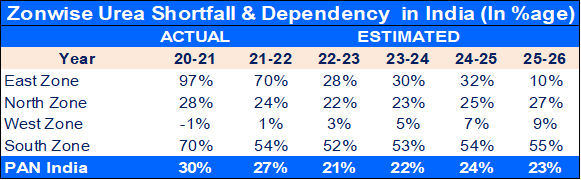

If we see zone wise dependency, East zone dependency will reduce from 97% to 10% in next 5 years with consideration of increased demand with a CAGR of 2.7%.

South zone will be focussed market where shortfall will be maintained around 55%, even after reduction in dependency by 15% from 70% to 55%, after commencement of Ramagundam urea production.

West zone will be comfortable in urea availability and dependency will slowly increase to a level of 9% in next 5 years from -1%.

Dependency will be around 25% in North zone in coming 5 years even after adding HURL Gorakhpur capacity which is expected to commission in Aug / Sept 2021.

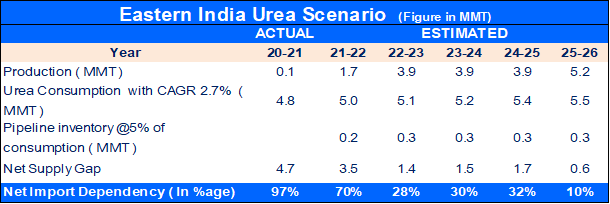

Eastern India Urea Scenario

Production capacity in eastern India is just negligible and totally depends on imports or on the other states. There was almost 97% gap in production and demand.

Out of 6 Urea Plants additions in India, 4 Urea plants (HURL, Matix & Talcher) are in Eastern States and will add 5.08 Mn tons, as against demand of 4.8 Mn tons in 2020-21. Is It true that eastern India will be in surplus position in future after adding these capacities?

Eastern India urea demand is increasing with a CAGR of 2.7%. Even after adding the capacity, shortfall between production and demand will be around 25 – 30% which will further reduce after commission of Talcher Urea plant by 22%.

Northern India Urea Scenario

North zone of India is the largest urea consumer in India with demand of 12.8 Mn tons and will touch a level of 14.1 Mn tons in next 5 years, with a CAGR of 2.06%. Production in north zone is 9.8 Mn tons, which will reach at 11.1 Mn tons with commissioning of HURL Gorakhpur plant by this year. Gap between production and demand will remain same i.e. around 25%.

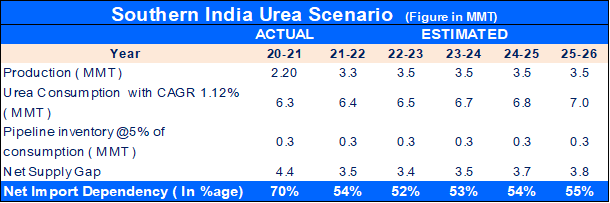

Southern India Urea Scenario

Net urea dependency on imports is 2nd highest in South zone with 70% after East zone i.e. 98%. Eastern zone shortfall will reduced drastically after HURL & Matix urea plant.

With commencement of production in Ramagundam urea plant, shortfall between production and demand will reduce from 70% to 54% in South zone of India and will remain at same level next 5 years.

South India require 3 additional capacity to fulfil gap of around 3.5 – 3.8 Mn tons.

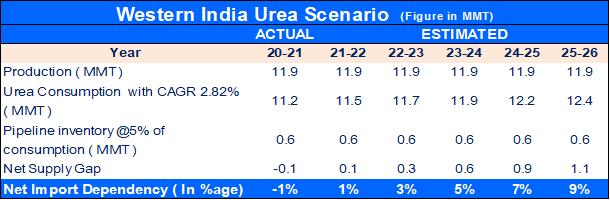

Western India Urea Scenario

Most comfortable zone in urea availability is West zone in India, as gap between production and demand is almost negligible i.e. at around -1% in 2020-21 and will reach by 9% in next 5 years.

West zone is 2nd highest consumer (after North zone) in India with demand of 11.2 Mn tons and will touch a level of 12.4 mn tons with a CAGR of 2.82% highest CAGR in India.

Factors of NPK consumption and population growth are not taken into consideration, which may also affect / increase urea demand growth with various government scheme promoting agriculture to ensure food security.

Looking to the urea demand growth for long terms, should India focus on long terms strategies right now and think on many scheme like liberalization in import permits for urea imports and promoting JVs in abroad under PPP or long term tie up for supplies to India etc.