In the intricate ecosystem of global agriculture, fertilizers serve as the lifeblood, enriching soils and nurturing crops to meet the world’s growing food demands. The dynamic relationship between fertilizer demand and production is a crucial aspect of agricultural sustainability and productivity worldwide.

On the production front, key fertilizer-producing countries like China, India, the United States, Russia, and others play a significant role. These countries harness natural resources and advanced technologies to meet both domestic and global fertilizer demand. However, production dynamics can be influenced by factors such as resource availability, environmental regulations, and geopolitical tensions.

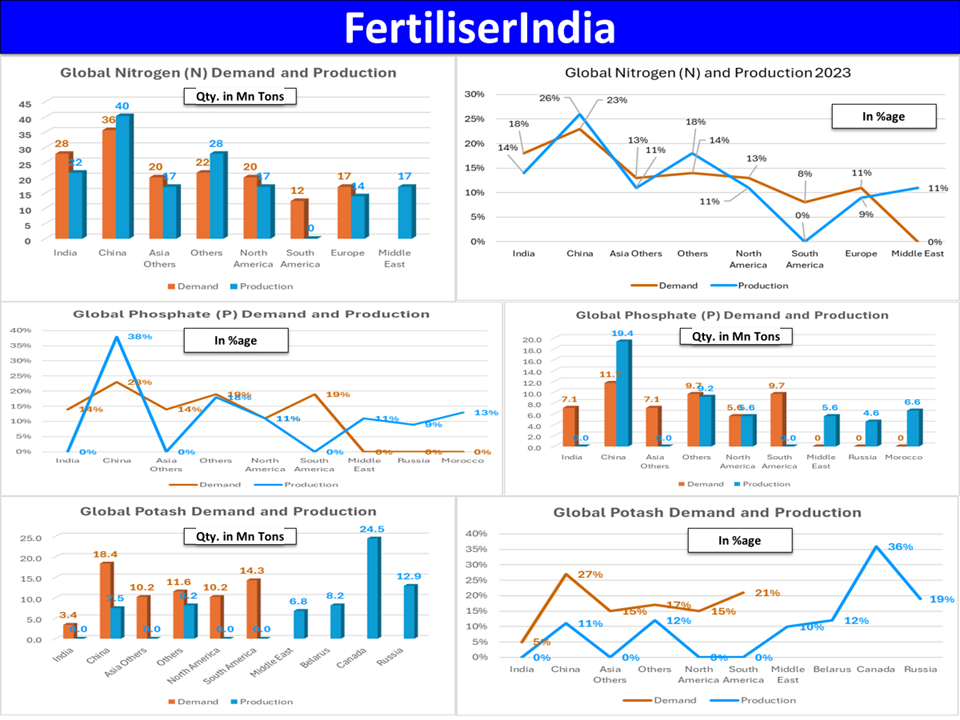

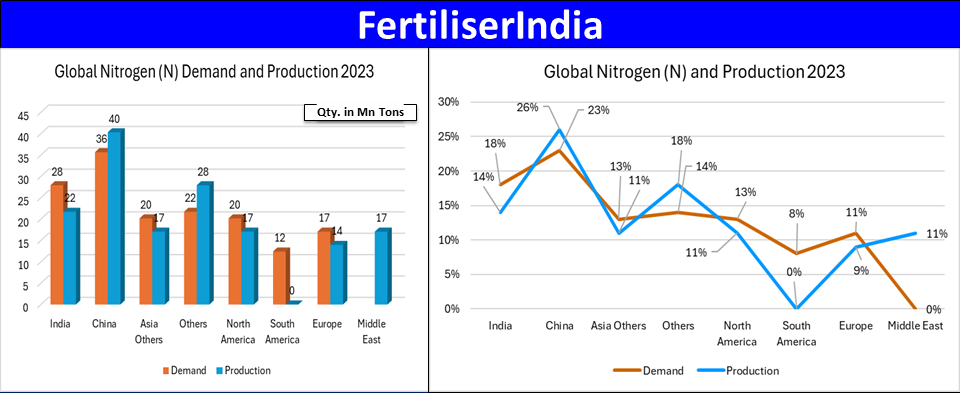

Global Nitrogen (N) Demand and Production

Nitrogenous fertilizers, crucial for crop growth, contain nitrogen, vital for protoplasm and photosynthesis. Comprising compounds like ammonium nitrate, ammonium sulfate, calcium ammonium nitrate, and urea, they’re applied alongside animal manure to enhance crop quality, boost flower differentiation, and accelerate shoot growth. These fertilizers are indispensable for modern agriculture, aiding in optimal crop yields and sustainable farming practices.

Among nitrogenous fertilizers, including urea, ammonium nitrate, ammonium sulfate, calcium ammonium nitrate (CAN), and others, urea emerged as the dominant segment, representing the largest share.

Urea, a widely used nitrogen fertilizer, is essential in modern agriculture due to its gradual nitrogen release, versatility across various crops, and cost-effectiveness. Its adoption spans diverse agricultural practices, appealing to farmers of all scales and driving market expansion.

The global nitrogen production and demand is centered in key countries, with China and India emerging as the largest producers and consumers, accounting for 26% and 14% of production respectively, and 23% and 18% of demand respectively.

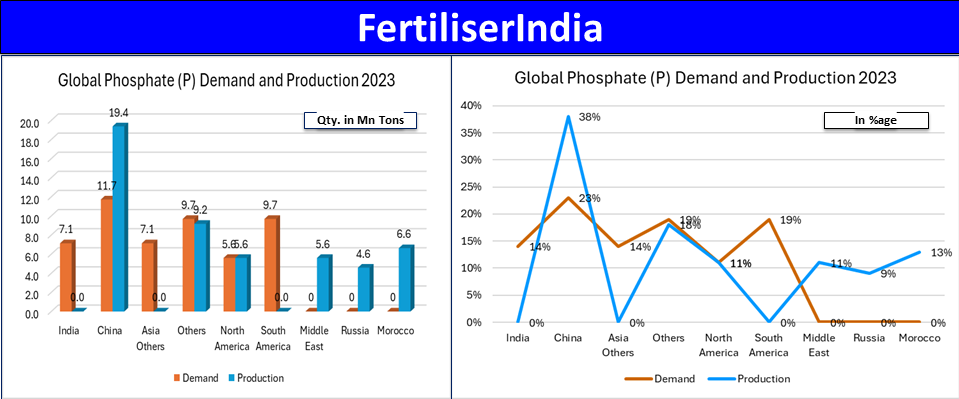

Global Phosphate (P) Demand and Production

Phosphate, a natural resource buried beneath the Earth’s surface, serves as a crucial element utilized across various agricultural and industrial sectors. The global phosphate market has been categorized into five distinct types: ammonium/phosphoric acid, calcium, potassium, sodium, and other derivatives.

The surge in fertilizer demand is largely driven by the reliance on naturally occurring phosphorus-containing minerals for the production of almost all phosphate fertilizers. Phosphorus (P), an indispensable nutrient in agriculture, has historically been essential for farming practices. However, phosphate in its natural state, like apatite mineral, isn’t readily absorbable by plants. Consequently, phosphate rock necessitates processing to transform phosphorus into soluble or plant-accessible forms, offering various pathways for fertilizer production.

In 2023, the Phosphate Market Size reached a valuation of USD 12.9 billion. This growth trajectory reflects a compound annual growth rate (CAGR) of 4.57%.

The global phosphate production is centralized in several key nations, with China, Morocco, and Russia emerging as the primary producers, commanding 38%, 13%, and 9% of the market share, respectively.

Major players in the phosphate industry include OCP Group from Morocco, The Mosaic Company from the US, EuroChem Group headquartered in Switzerland, Nutrien Ltd based in Canada, Jordan Phosphate Mines Co. from Jordan, ICL Group Ltd from Israel, PhosAgro from Russia, Ma’aden-Saudi Arabian Mining Company from Saudi Arabia, Yara International ASA from Norway, Innophos Holdings, Inc. from the US, and Yunnan Phosphate Haikou Co., Ltd. (YPH) from China.

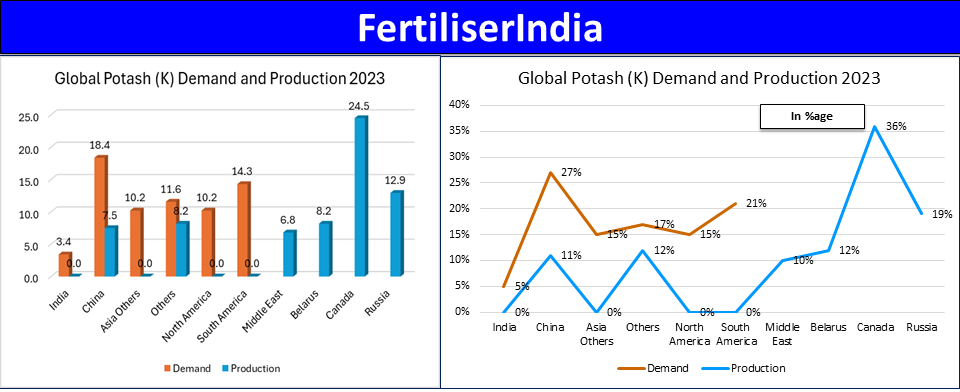

Global Potash (K) Demand and Production

The global potash market holds immense importance in agriculture, serving as a vital nutrient essential for robust plant growth. This dynamic market is shaped by a myriad of factors, including agricultural demand, fluctuations in fertilizer prices, and mining production. Major players in potash production, such as Russia, Canada, and Belarus, wield significant influence, while behemoth consumers like China and India drive substantial market activity. Market trends are subject to the ebb and flow of agricultural cycles, the sway of geopolitical factors, and the transformative impact of technological advancements in farming practices.

The global stage of potash production is spotlighted by a select few nations, where Canada leads the pack with a commanding 36% share, followed by Russia at 19% and Belarus at 12%. These nations boast abundant reservoirs and cutting-edge mining infrastructure tailored for the extraction of this essential agricultural resource.

In Canada, particularly in Saskatchewan, some of the world’s largest potash mines are operated by industry giants like Nutrien and Mosaic. Russia, through companies such as Uralkali and EuroChem, also commands a significant presence in global potash production, leveraging deposits in the Ural Mountains and the Volga region. Belarus, represented by firms like Belaruskali, emerges as another heavyweight in the global potash arena, boasting extensive reserves in the Soligorsk and Lyuban regions. While countries like China, Germany, and the United States also contribute to global potash production, their impact is comparatively modest when juxtaposed with the dominance of the aforementioned key players.

The global potash production scene is defined by a handful of major players, abundant reserves, and substantial investments in mining infrastructure. Production levels in these countries can be swayed by market dynamics such as demand and price fluctuations, alongside geopolitical influences.