Ukraine suspended seaborne imports of ammonia-based fertilizers through its Black Sea deep-water ports, citing elevated risks of industrial accidents amid the ongoing Russia’s attacks. The move had already disrupted the existing supply chains, driven the fertilizer prices to new highs, and cast uncertainty over Ukraine’s production and export potential next 2026/27 season.

In the letter dated July 7, 2025, addressed to the Ukrainian Sea Ports Authority (USPA), Vice Admiral Neizhpapa, the Commander of Ukraine’s Naval Forces, recommended the ships carrying hazardous materials not to enter the Ukrainian territorial waters and the ports to prevent potential explosions caused by Russia’s missile and drone strikes on ships, vehicles, or storage facilities containing explosive substances. The recommendation specifically targets anhydrous ammonia, ammonium nitrate, ammonia solutions, and mixtures containing explosive compounds. The Ukrainian ports have already completely suspended receiving and unloading of such cargoes since mid-July, despite the advisory nature of the letter.

The importing companies have begun rerouting ships to alternative ports in Moldova (Giurgiulești) and Romania (Galați), while also exploring the option of land-based deliveries, including rail transport from the EU countries. However, these alternatives seemed to face serious capacity constraints and higher logistics costs, a burden that ultimately falls on farmers.

“For example, transshipment costs in Romania’s port of Galați can total up to €10 per tonne depending on the operator, and this directly drives up the fertilizer price,” a Ukraine-based dealer said.

In early August, ammonium nitrate prices in Ukraine rose to UAH24,500 per tonne on DAP-western border crossing point basis, up 17% compared to April and nearly 30% above the level seen during the same period last year, according to data from the Ukrainian news agency Infoindustria.

Since mid-July, restrictions on unloading ammonium nitrate and ammonia at the Ukrainian Black Sea deep-water ports, along with rising nitrogen fertilizer prices, put significant pressure on the farmers ahead of the 2026/27 autumn sowing season off to start in late August-mid-September.

For many Ukrainian farmers, especially small and medium-sized producers, rising logistics costs would make fertilizers less affordable. In April 2025, Ukraine’s Fertilizer Affordability Index (FAI), calculated by LSEG Agriculture Research, based on fertilizer prices to grain quotes ratio, set at 0.52, but by August it had declined to 0.44, reflecting a 15% drop in affordability over just a few months. This downward trend signals growing economic pressure on farmers, as FAI value below 1.0 indicates that fertilizers are economically unaffordable, meaning input costs outweigh the potential revenue from crop sales.

| January 2025 | April 2025 | August 2025 |

| 0.49 | 0.52 | 0.44 |

Table 1

Ukraine. Fertilizer Affordability Index, 2025

Source: LSEG Agriculture Research calculations

“We have already started to review our fertilizer purchase plans. We are not too sure about the autumn sowing campaign with rising prices and limited fertilizer supply,” one farmer based in the Kyiv region said.

As a result, many Ukrainian farmers preferred to postpone fertilizer purchases, expecting grain prices to rise and allow them to sell their crops with a higher margin to buy fertilizers closer to the 2026/27 sowing season in September or October. Ukrainian 11.5% protein wheat prices on a CPT-Odesa basis rose to $226 per tonne by August 11, 2025, 10% higher compared to $206 recorded on June 20 as a 9-month low, according to LSEG’s records. RIC: KTS-W11UABS-CPT

“Currently, fertilizers are being purchased primarily by large agricultural holdings that can afford early payments to diversify supply risks,” a Ukraine-based fertilizer trader confirmed.

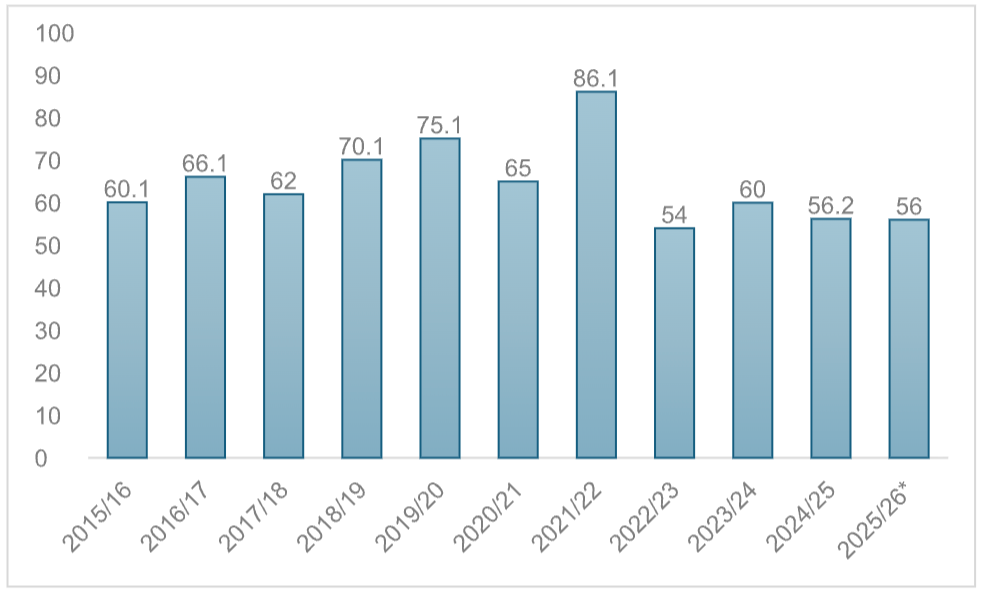

The crops requiring the higher levels of nitrogen fertilizers applied, including winter wheat, corn, and rapeseed, expected to be among the most affected by the fertilizer shortage from August 2025 onwards. Nitrogen deficiency may lead to slower plant growth, lower yields, and worser quality of Ukrainian grains next 2026/27 season, running from July to June. Ukraine’s Economy Ministry raised its 2025 grain forecast to 56.0 million tonnes, driven by a stronger corn harvest up to 28.0 million tonnes, while wheat production estimate remained at 21.0 million tonnes. Ukraine’s 4-year average grain output since 2022, when Russia invaded Ukraine, slid to 56.5 million tonnes from 74.0 million tonnes between 2018 and 2021.

Chart 1

Ukraine. Grains and pulses production, 2015-2025, in million tonnes

Source: Ukraine’s State Statistic Services’ data https://www.ukrstat.gov.ua/

Ukraine’s domestic fertilizer production tried to help stabilize supply, while operating under highly insecure conditions related to Russia’s wartime disruptions and halts in maritime imports. In the first half of 2025, OSTCHEM’s Rivneazot increased output, offsetting declines at Cherkasy’s Azot, caused by Russia’s drone attacks and energy shortages afterwards whereas the group’s January-June 2025 output inched down. Both plants resumed operations in late May, and the company is working to increase its energy independence to ensure stable supply for Ukrainian farmers.

In the first half of 2025, fertilizer production at Ostchem’s plants decreased by 7.47%, totaling 849,900 tonnes, compared to 918,500 tonnes in the same period of 2024. The most significant decline was recorded at Cherkasy Azot plant, where output dropped by 21% to 567,100 tonnes. Meanwhile, Rivneazot’s production showed a positive trend, increasing production by 40.9% to 282,700 tonnes, partially offsetting the overall decline across the group, according to a statement from Group DF, currently representing the sole fertilizer production facilities in Ukraine.

| Commodity | 1H 2024 | 1H 2025 | Change (%) |

| Total Production | 918.5 | 849.9 | -7% |

| Cherkasy Azot | 718.0 | 567.1 | -21% |

| Rivneazot | 200.7 | 282.7 | +41% |

Table 2

Ukraine. Osthem’s fertilizer production, 2024-2025, in 1,000 tonnes

Source: Osthem’s company data

A potential decline in crop yields in the next 2026/27 production cycle combined with rising production costs might reduce Ukraine’s grains and oilseeds export potential and weaken the country’s position in the international markets, leading to smaller foreign currency inflows, especially amid the ongoing Russia’s war and restricted access to port infrastructure.

Article Written By: –

Iryna Prodan

Senior Research Specialist, Agriculture – LSEG Data & Analytics

Iryna Prodan is an experienced agricultural market analyst with over 15 years of expertise in the EU and Ukrainian markets. She specializes in fertilizer price assessments—particularly ammonium nitrate and urea—as well as grains, oilseeds, and vegetable oils across the EU and South America. At the London Stock Exchange Group, she delivers daily insights and independent research that support strategic decisions in agribusiness, focusing on supply-demand dynamics and pricing trends.

📍 Based in Gdynia, Poland

📧 Iryna.Prodan@lseg.com