India, one of the world’s largest consumers of fertilizers, continues to rely heavily on imports to meet its agricultural demand. The data on country-wise fertilizer imports during 2024–25 highlights not only the scale of dependence but also the changing dynamics of supply sources.

Fertilizer Imports by Category (2024–25)

(Figures in Lakh MT)

| Fertilizer Type | Total Imports (LMT) | Key Supplier Countries |

|---|---|---|

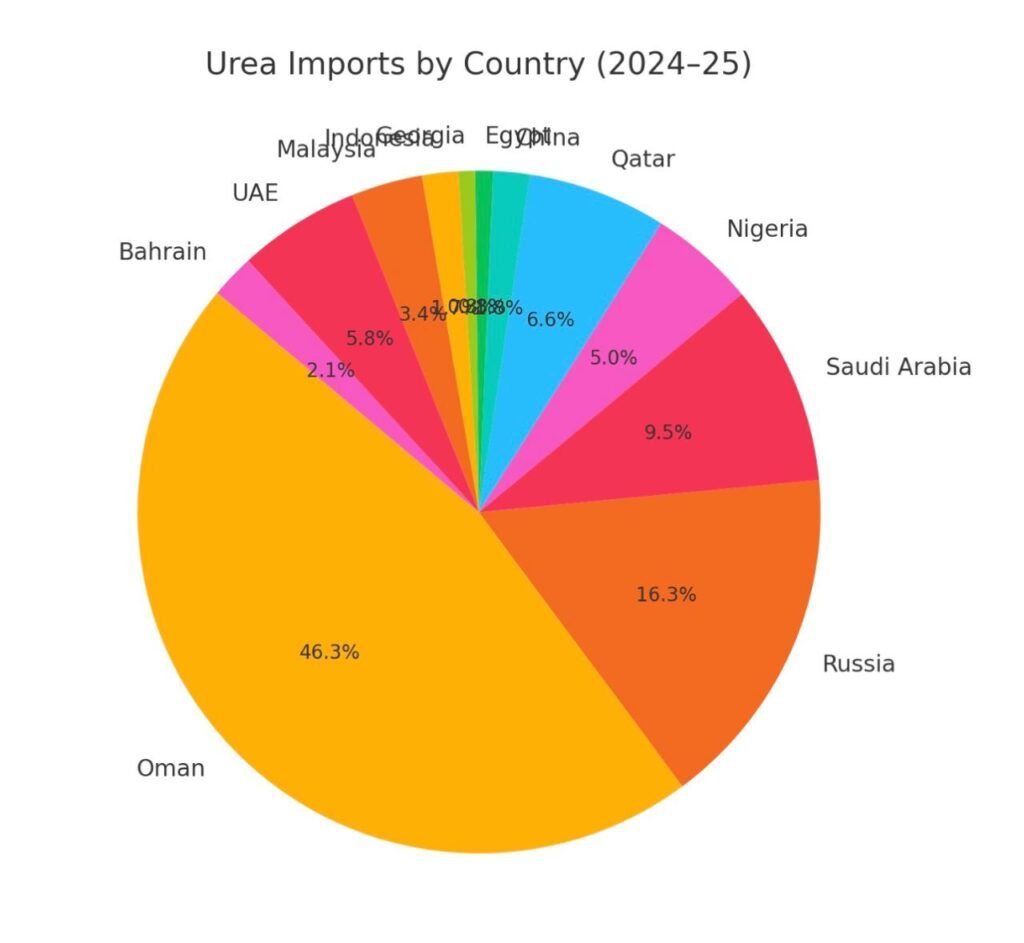

| Urea | 56.47 | Oman (26.13), Russia (9.23), Saudi Arabia (5.38), Nigeria (2.83), Qatar (3.70) |

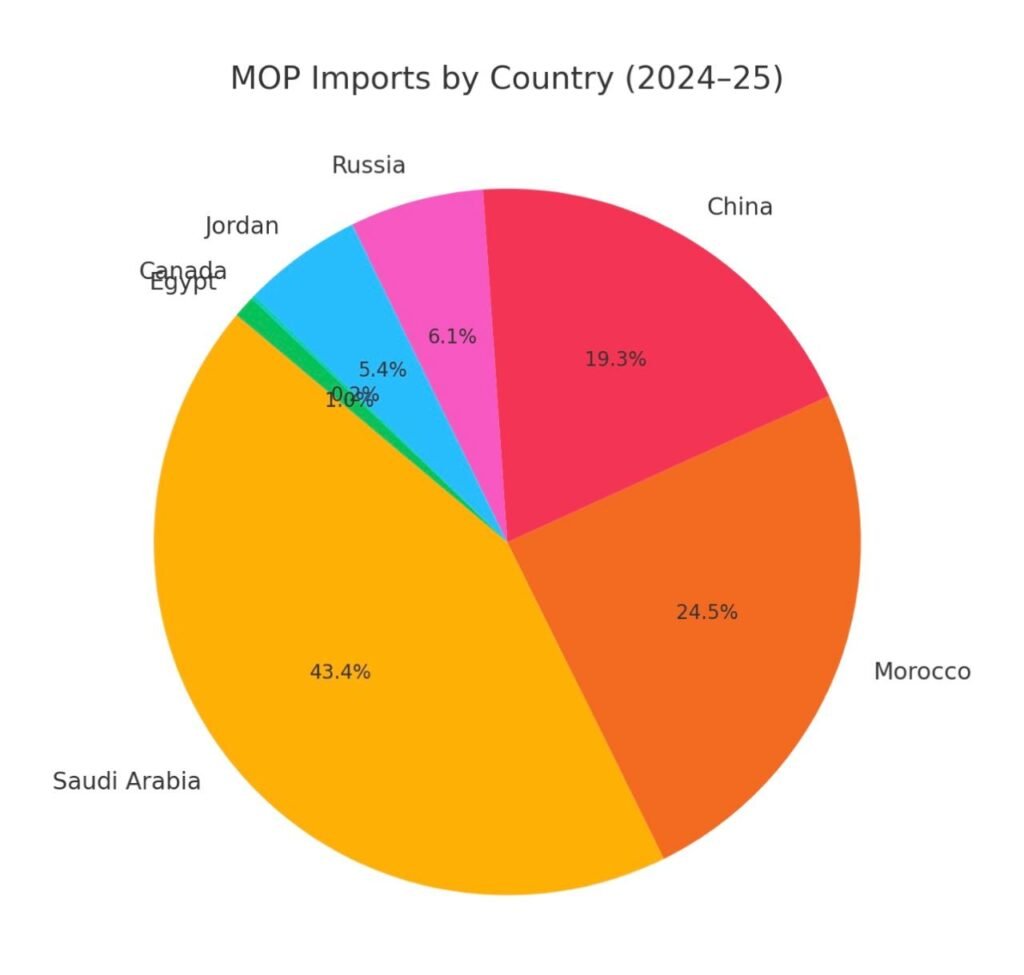

| MOP – Muriate of Potash | 45.69 | Saudi Arabia (19.05), Morocco (10.74), China (8.47), Jordan (2.39), Russia (2.69) |

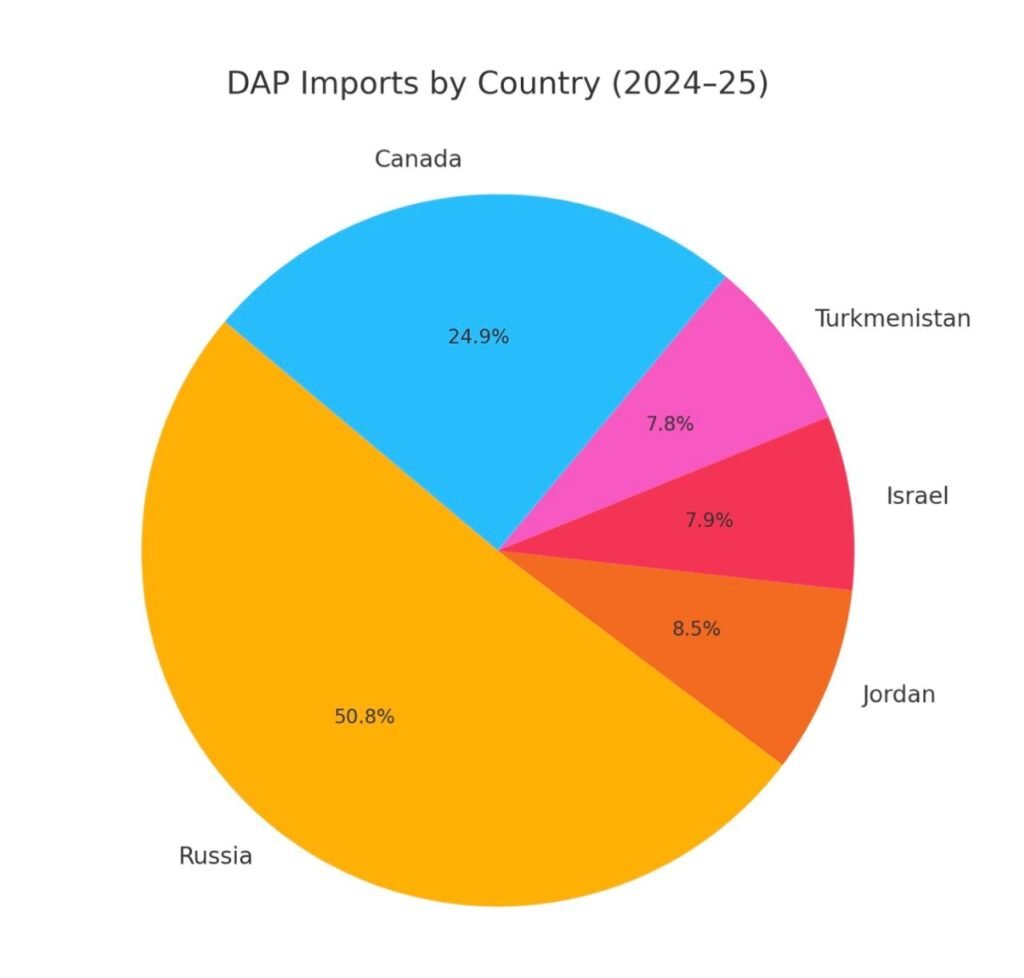

| DAP – Di-Ammonium Phosphate | 35.41 | Russia (18.00), Jordan (3.01), Israel (2.80), Turkmenistan (2.77), Canada (8.83) |

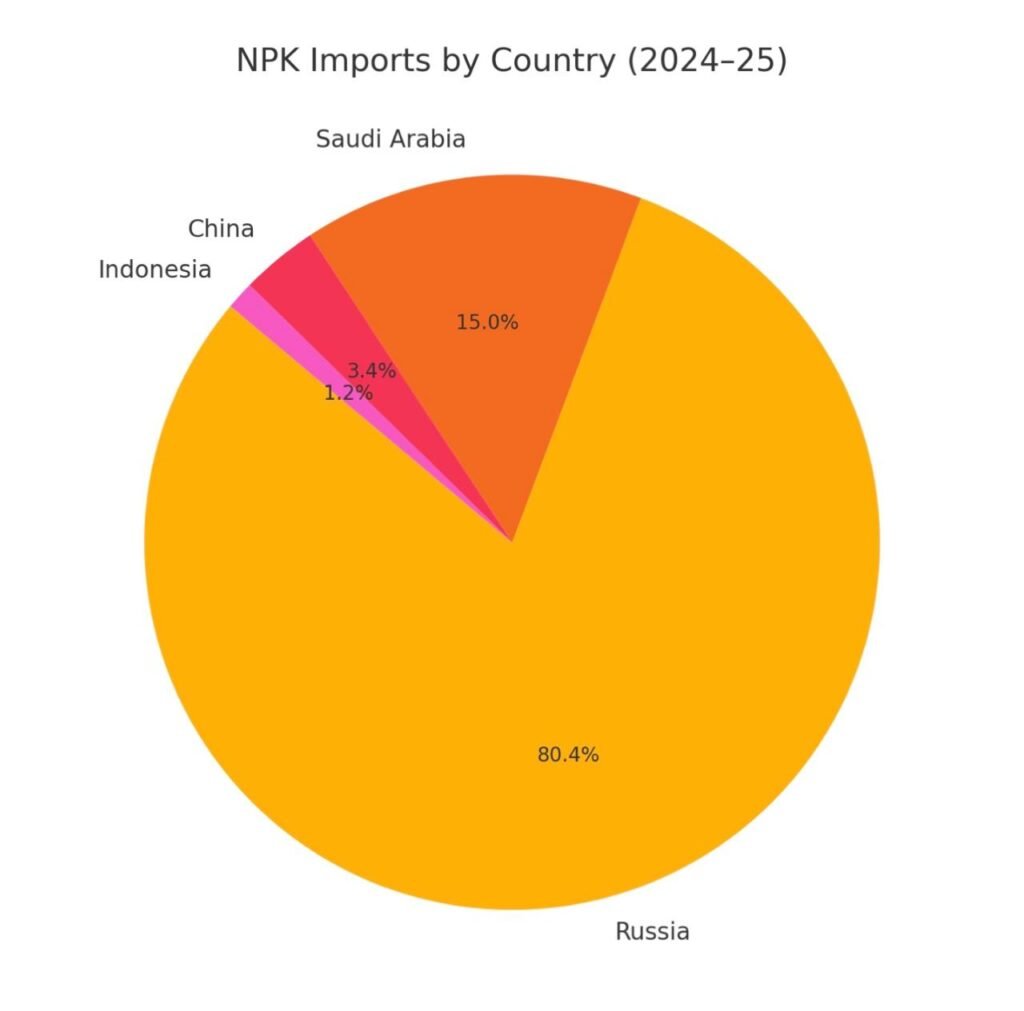

| NPK | 22.72 | Russia (18.27), Saudi Arabia (3.40), China (0.77), Indonesia (0.28) |

Key Highlights:

1. Urea Dependency on Oman

With 46% of India’s Urea imports coming from Oman, strategic relations in the Gulf remain crucial for India’s food security. Russia and Saudi Arabia follow, together contributing over 25% of the supply.

2. Potash Dominated by Saudi Arabia & Morocco

MOP imports are led by Saudi Arabia (42%) and Morocco (24%), reflecting India’s increasing outreach to the Middle East and North Africa (MENA) for potash.

3. Russia Emerges as a Multi-Sector Supplier

Russia’s dominance is notable—it supplies across all four categories, accounting for 18 Lakh MT of DAP and 18.27 Lakh MT of NPK, making it India’s single most diversified fertilizer partner.

4. Diversification vs. Concentration Risks

While India is engaging multiple partners, high concentration in specific regions (Oman for Urea, Saudi Arabia for Potash) creates vulnerability. Geopolitical disruptions or trade restrictions could directly impact agricultural stability.

• Supply Security: India needs to balance between Gulf, CIS, and African suppliers to reduce over-reliance on a few nations.

• Logistics & Freight: With freight volatility, sourcing from nearby Gulf countries ensures cost competitiveness.

• Policy Direction: Strengthening joint ventures in fertilizer plants abroad—especially in Oman, Russia, and Africa—can provide long-term security.

• Sustainability Angle: Alongside imports, domestic production and green ammonia initiatives could gradually lower external dependency.

The 2024–25 fertilizer import data reflects both strengths and vulnerabilities in India’s agricultural input strategy. While partnerships with Oman, Russia, and Saudi Arabia remain pillars of supply, diversifying trade routes and investing in local capacity will be critical to ensuring stable, sustainable, and affordable fertilizer access for India’s farmers.