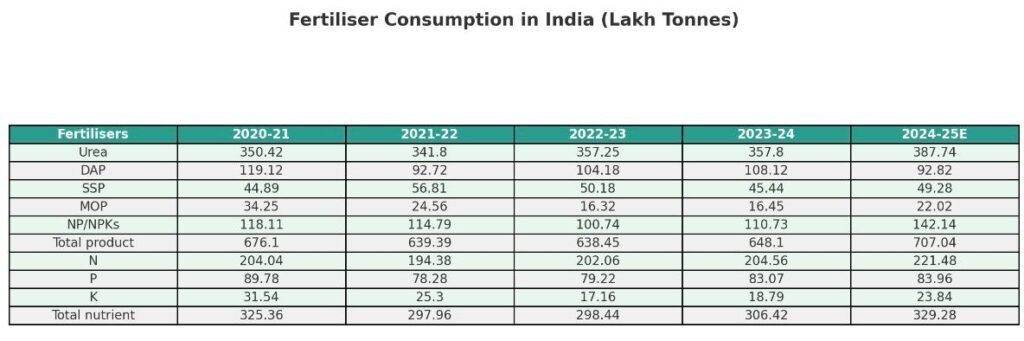

India’s fertiliser consumption patterns in 2024–25 reveal not just incremental growth, but a fundamental realignment in the nation’s agricultural input dynamics. With total consumption expected to surge to 70.7 million tonnes, an impressive 9.1% rise over last year, the data narrates a story of both resilience and recalibration.

Urea: The Unshakable Backbone

At 38.77 million tonnes, Urea consumption has risen 8.4% over last year. Its affordability and the government’s subsidy regime keep it firmly entrenched as the backbone of Indian agriculture. Yet policymakers are cautious—excessive nitrogen use risks eroding soil health and long-term productivity. The surge in Urea highlights both India’s dependence and the pressing urgency of diversification.

DAP: A Strategic Decline

In sharp contrast, Diammonium Phosphate (DAP) has declined 14.2%, slipping to 9.3 million tonnes. Far from being a setback, this drop reflects a strategic correction. High global prices and farmer sensitivity have nudged consumption downward, reinforcing the need for balanced phosphorus use. The fall also indicates growing acceptance of affordable alternatives that deliver comparable nutrient value.

SSP and MOP: Affordable Allies

As DAP recedes, Single Super Phosphate (SSP) and Muriate of Potash (MOP) are stepping into the spotlight. SSP, the low-cost phosphorus fertiliser known as the “farmer’s fertiliser,” grew 8.5% to nearly 5 million tonnes. Meanwhile, MOP, critical for potash-deficient Indian soils, has staged a 33.9% comeback, crossing 2.2 million tonnes. Together, they mark a long-overdue correction in India’s soil nutrition practices.

NP/NPKs: The Game-Changer

The most striking trend is the meteoric rise of complex fertilisers (NP/NPKs, excluding DAP/MAP). Consumption is expected to soar 28.4%, surpassing 14.2 million tonnes. This signals a decisive turning point: farmers are adopting balanced blends that provide nitrogen, phosphorus, and potassium in the right proportions. Complex fertilisers are no longer peripheral—they are becoming the central force in India’s nutrient management strategy.

Nutrient Balance: Towards Sustainability

From a nutrient perspective, the shift is unmistakable. Nitrogen use will rise 8.3%, maintaining its lead. Phosphorus use remains almost stable, with a modest 1.1% gain. The most remarkable change is in potash (K), which will surge 27%, reflecting long-overdue recognition of India’s potash-deficient soils. Total nutrient use is expected to grow 7.5%, crossing 32.9 million tonnes. The data underscores a clear move towards a balanced N-P-K profile, a cornerstone of sustainable agriculture.

From Volume to Value: The Big Picture

India’s fertiliser story is no longer just about chasing volumes. The decline in DAP, the revival of MOP, and the surge in NP/NPKs point to a maturing market—one that values balance over bulk. Farmers are beginning to view fertilisers not merely as yield enhancers but as strategic investments in soil health, productivity, and profitability.

For policymakers, this transformation highlights the success of awareness campaigns, balanced fertilisation drives, and subsidy reforms. For businesses, it opens vast opportunities in specialty nutrients, bio-stimulants, customised blends, and green fertiliser technologies. For India’s agriculture, it represents a bold evolution, aligning with global sustainability goals while fortifying national food security.

India’s fertiliser consumption in 2024–25 is not just a statistic—it is a statement of intent. The nation is shifting decisively from quantity-driven expansion to quality-focused sustainability, with an unshakable focus on soil balance, farmer resilience, and agricultural competitiveness on the global stage.