As 2025 nears its close, global commodities and freight markets are caught in a storm of volatility, policy pressure, and structural imbalance. Fertilizer prices remain unsettled, freight is grappling with overcapacity, and dry bulk markets show sharp regional contrasts. For global businesses, this is not simply a cycle, it is a test of agility and strategy.

Nitrogen: A Market Losing Ground

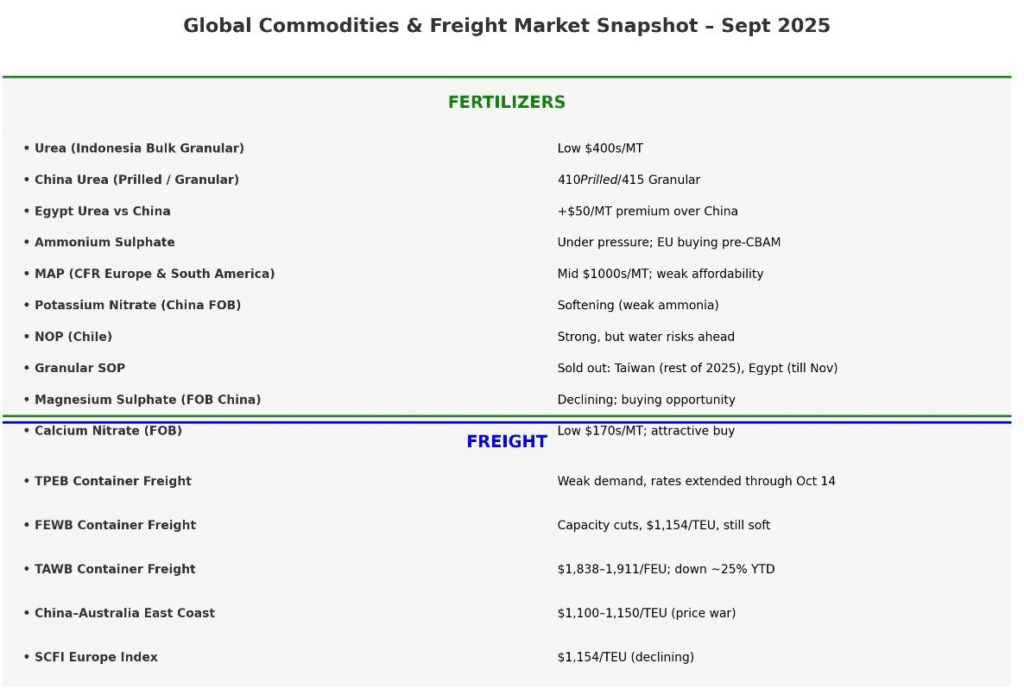

The nitrogen market is showing signs of fatigue. Indonesian granular urea has slipped into the low $400s FOB, while China’s artificial price floors—$410 for prilled, $415 for granular—are holding the line without solving underlying weakness. Quotas are limited, smaller cargoes remain difficult to source, and Egypt’s urea is trading at a $50/MT premium.

Ammonium sulphate is under particular strain as European buyers race to secure product before the January 2026 CBAM deadline. With Chinese CIQ quota applications due by September 30, the risk of shipment delays beyond deadlines further clouds the outlook.

Phosphates: Stability with a Fragile Core

Phosphates present a rare balance: technical MAP prices remain in the mid-$1000s CFR Europe and South America. But this apparent stability masks two opposing realities—tight supply on one side, and weak farmer affordability on the other. The closure of China’s export window next week could disrupt the balance, creating fresh waves of price volatility.

Potassium: Substitution Underway

The potassium market is being reshaped by substitution. Chinese potassium nitrate has softened as ammonia weakens, while Chile’s NOP remains firm but exposed to water risks.

High-priced SOP is driving buyers in chloride-tolerant regions to switch toward soluble MOP. Yet, availability is tight: Taiwan’s granular SOP is sold out for the year, and Egypt is booked until November. Uzbekistan is offering the cheapest prices, but geopolitical risks—particularly transit via Iran—dampen enthusiasm.

Secondary Fertilizers: Tactical Buying Windows

Not all markets are bleak. Magnesium sulphate prices have fallen FOB China, with favorable freight rates creating a strong buying opportunity. Calcium nitrate remains steady at the low $170s FOB, but analysts expect prices to firm within two to three months as China prioritizes domestic supply. Kieserite, meanwhile, has become tighter, widening its premium over heptahydrate by $20–30/MT.

Container Freight: Rates Under Siege

Global container markets are in retreat.

• Trans-Pacific Eastbound (TPEB): No Golden Week surge; carriers extend current rates into October.

• Far East Westbound (FEWB): Even with 25% of capacity blanked, the SCFI Europe index has fallen to $1,154/TEU.

• Trans-Atlantic Westbound (TAWB): Despite congestion at major North European ports, spot rates to the US East Coast have fallen ~25% year-to-date.

• Australia/New Zealand: Intense price wars have driven rates from China to Australia East Coast as low as $1,100/TEU.

Dry Bulk: Divided by Region

The dry bulk market shows a fragmented picture:

• Asia is softening, though steel cargoes remain a bright spot.

• The Indian Ocean is weighed down by monsoons and political tension.

• The Atlantic Basin is firmer, with the US Gulf strong on Handysize demand and Europe pulling tonnage westward.

The global trading environment is no longer defined by uniform trends, it is shaped by fragmentation and volatility. Fertilizer buyers face artificial price floors, quota restrictions, and affordability gaps. Freight markets are battling oversupply and pricing wars.